E-invoicing mandates and AP automation: why compliance is not enough

A recap of the Shared Services Link webinar co-hosted with Springtime Technologies and Avalara, June 2026

When Poland’s KSeF mandate went live on February 1st this year, nearly 300 million B2B electronic invoices were processed in the first four months alone. Belgium, which went live on January 1st, now has over 1.1 million companies registered on Peppol. These are significant volumes. They are also, in a narrow sense, success stories: the infrastructure held, the invoices moved, the governments got their data.

What those numbers do not tell you is what happened inside AP departments on day two.

That was the subject of a webinar hosted June 10th 2026 by sharedserviceslink in association with Springtime Technologies, with additional expertise from Avalara. The conversation brought together Accounts Payable (AP) leaders from large multi-entity organizations, many of whom had been through the Poland go-live and are already planning for France. The central argument, and the one that generated the most discussion, was this: a mandate makes an invoice legally compliant but, critically, it does not make that invoice ready for your ERP.

What e-invoicing mandates really validate versus what they leave out

- Supplier ID

- VAT number

- the arithmetic relationship between net, VAT, and gross amounts

- the application of correct tax codes

Those are the conditions for compliance, and an invoice that passes them is, from the government’s perspective, complete. From an AP department’s perspective, it is often missing most of what really matters. We’re talking about things like PO number, GL code, cost center, unit of measure, delivery note number, internal product codes: none of these are mandatory fields under most national mandates. Governments do not require them because tax authorities don’t need them to do what the mandates are in place to enforce. But AP teams do, because without them the invoice cannot be matched and posted without manual intervention. Jason Palmer, Senior E-Invoicing Sales Executive at Avalara, made the operational implication precise: if a supplier has always formatted their PO reference as the last six digits of a number your ERP expects in full, you need a process that recognizes that pattern and corrects for it. Compliance infrastructure does not do that. The mandate creates the invoice. Something else has to make it workable.

What the KSef go-live taught AP teams: evidence from the Poland mandate

The webinar polled its audience on their experience with the Poland go-live. 87% described it as manageable but said it had added extra work. A further 12% said they expected efficiency gains to materialize eventually. A small number reported they were still fixing problems.

Nobody said it was straightforward.

These are AP professionals at organizations that had invested years in supplier enablement, data quality programs, and automation infrastructure. While the mandate did not undo all of that, it did disrupt it enough that most teams absorbed additional work, and the efficiency gains many anticipated from moving to structured electronic invoicing had not yet materialized by the time of this webinar.

The reason, as Steve Standring (CRO at Springtime) explained, is that organizations which have spent 20 years getting suppliers to send data in the exact format their ERP requires are the ones most exposed. Because a new mandate impacts this delicately curated format significantly. Some of the configuration work those teams had done, PO flips, custom API mappings, supplier-side data transformation, no longer applies once invoices route through a government gateway.

Why e-invoicing compliance is an ongoing operational commitment, not a one-off project

Italy introduced its SDI mandate in 2019 and since then, the Italian mandate has gone through 40 documented changes, covering document type codes, cross-border AP reporting requirements, and numerous other adjustments. The point Jason raised was not that Italy is uniquely complex but that no mandate is a fixed goalpost.

This matters for how organizations approach the problem. Teams that treat each country as a separate compliance project, solved once and moved on from, accumulate fragmentation: multiple vendors, inconsistent exception-handling processes, and no shared intelligence across markets. The organizations managing this well, according to both Steve and Jason, are treating it as a continuous operational program.

To put it another way, successful companies think of the compliance deadline as the starting line, not the finish.

France e-invoicing mandate September 2026: what AP teams need to know

The next significant deadline for global enterprises will be France. From September 1st 2026, large and mid-sized companies must issue and receive structured e-invoices through a certified Plateforme Agréée (PA). Unlike Italy’s single government portal or Belgium’s Peppol-based model, France uses a decentralized Y-model, where each business selects and integrates with its own accredited platform.

That choice carries AP consequences that are easy to underestimate. A platform that handles Accounts Receivable (AR) compliance cleanly but has limited capability around AP data enrichment will create the same compliance-efficiency gap described throughout the webinar, just in a new country. Steve noted this risk specifically in the context of the UAE mandate, where a single accredited provider must handle both AR and AP flows: selecting a vendor on compliance credentials alone, without evaluating AP automation depth, is where problems can begin.

The second webinar poll found that 40% of attendees are approaching mandate preparation through a strategic transformation program while 25% are still handling it tactically, country by country. The tactical approach is not necessarily wrong for organizations with limited mandate exposure. For enterprises managing invoice volumes across 10 or 15 markets, it creates a fragmentation problem that becomes very expensive to untangle.

AI in AP automation: where it makes a measurable difference and where the risks live

The conversation included a candid segment on AI’s role in AP, which is worth relaying accurately because the market conversation around this topic tends toward the optimistic.

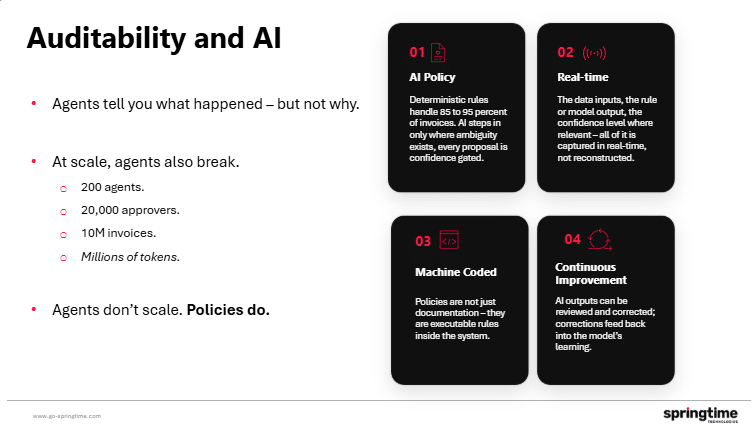

The area where AI is making a measurable difference right now is data enrichment and matching. Springtime’s Invoicetrack, which processes invoices from government gateways alongside PDFs and email attachments, uses 18 months of historical invoice data to train matching logic specific to each supplier’s behavior. That means the system can recognize non-standard PO formats, populate missing GL codes, unpack single-line purchase orders that return as multi-line invoices, and flag duplicate payments, including the hotel invoice that arrives through the gateway after a credit card payment has already been processed. According to Steve, mature deployments within Springtime’s customer-base are reaching 80%+ touchless processing rates. For context on what that means in practice: across the broader market, average AP operations process around 8,000 invoices per FTE annually, while world-class operations reach over 40,000. The gap between those two figures can be largely attributed to how the right partner helps you anticipate and respond to exceptions that degrade your otherwise potential-filled straight-through rate.

The more cautious note concerned agentic AI. If autonomous agents are resolving exceptions across millions of invoices, they produce a record of what they did, but not an explanation of why. In a finance context where every posting decision has audit and tax implications, that is a meaningful governance gap. The approach Springtime described instead uses agents to analyze historical data and generate human-readable policies, which are then compiled into deterministic machine-executable rules. The rules run at processing speed, use minimal computing power, and produce a fully auditable trail because every invoice category is treated consistently and the policy document explains the logic.

The distinction is between AI that makes opaque decisions at scale and AI that encodes human-reviewed judgment into transparent, repeatable processes. For AP teams that answer to internal audit and external tax authorities, the difference really can’t be understated.

How to prepare for an e-invoicing mandate go-live: the AP readiness framework

The practical framework Steve outlined for organizations approaching a mandate go-live can be summarized as:

Pre-go-live, the most valuable investment is training the matching system on existing invoice data so that common supplier patterns are already handled on day one. This does not eliminate exceptions after go-live, but it reduces the spike significantly. 60% to 80% of the matching issues that arise on day one, according to Springtime, can be resolved automatically if the system has been trained on the right historical data beforehand.

Post-go-live, the priority is process mining: understanding which suppliers are generating the most exceptions, which data fields are most frequently missing or malformed, and where AP staff are spending disproportionate time relative to invoice volume. That visibility is what makes continuous improvement a structured program rather than a series of one-off fixes.

The organizations Springtime and Avalara described as managing this well share one operational characteristic: they brought finance, AP, tax, legal, and IT into the same room before the mandate deadline, not after. This because the mandate of course, affects all of those functions. Invoice data questions are not purely an AP problem, tax validation is not purely a legal concern, and ERP integration decisions have consequences that IT cannot resolve in isolation. Teams that siloed the preparation work are the ones now coordinating cross-functional fixes under time pressure.

The Billentis 2026 report on global e-invoicing: key findings for AP teams

The Billentis 2026 report, titled “Riding the Tornado,” provides useful external context for the scale of what is coming. In 2019, roughly one in 10 invoices sent globally was truly electronic. That figure has now reached approximately three in 10, and the mandate pipeline from countries either live or committed by 2030 will continue to drive that number upward. The report’s title references the progression from the previous edition, “Watch the Tornado,” to the current phase where organizations are no longer observing in anticipation but are now actively participating in it.

The framing that resonated in the webinar was this: the organizations that absorbed the Poland go-live with the least disruption had already done the analytical work to understand what their ERP actually required versus what the mandate would deliver. That gap analysis, done in advance, is what separates a manageable go-live from one that adds months of remediation work.

Frequently asked questions on e-invoicing

Does e-invoicing automation work with SAP and Oracle?

Yes. Springtime’s Invoicetrack platform connects to SAP, Oracle, Microsoft Dynamics, and multi-ERP environments. The core integration points, vendor master data, PO data, and approval routing, are consistent across ERP systems, so the platform can be configured regardless of which ERP or combination of ERPs a business runs.

What data does an e-invoicing mandate actually require on an invoice?

National mandates require a legally compliant set of fields: supplier ID, VAT number, invoice totals, correct tax codes, and the prescribed format for that country. They do not require the operational fields AP teams need for automated matching, such as PO numbers, GL codes, cost centers, or unit of measure. That gap between legal compliance and AP readiness is the core operational challenge.

How many changes has Italy’s e-invoicing mandate gone through since 2019?

40 documented changes, covering document type codes, cross-border AP reporting requirements, and other adjustments. Italy’s SDI mandate is the most mature in Europe and illustrates why e-invoicing compliance is an ongoing operational commitment rather than a one-time implementation.

What is the difference between compliant e-invoicing and AP-ready e-invoicing?

A compliant invoice satisfies the tax authority’s validation rules and can be legally accepted. An AP-ready invoice contains all the data fields an AP team needs to match it against a purchase order, post it to the correct GL account, and process it without manual intervention. Most mandates produce the former. Getting to the latter requires data enrichment, supplier behavior mapping, and matching logic built on top of the compliance layer.

When does the France e-invoicing mandate take effect?

From September 1st 2026, all VAT-registered businesses in France must be able to receive structured e-invoices, and large and mid-sized enterprises must also issue them through a certified Plateforme Agréée. Small and micro-enterprises follow from 1 September 2027.

Readers should verify current requirements with qualified legal or tax counsel, as mandate timelines are subject to change

Would you like to keep the conversation going?

If you are preparing for France in September, or working through the implications of a mandate already live in your operating markets, Steve and the Springtime team are available for a conversation that involves no pitch decks or brochures. The offer is a working discussion about where the compliance-efficiency gap is likely to hit your specific AP operation and what preparation looks like in practice.

You can reach the team by clicking here.

And the full webinar recording is available to watch on demand over on sharedserviceslink.com.